The US Tax Code and the Code of Federal

Regulations show that income for most Americans is "excluded, or

eliminated for federal income tax purposes." You can easily see

this with a computer because the Income Tax has been codified.

TEXT/HTML

version (a repaired copy of the broken original from the GPO, the

most accurate, search it on your computer). PDF

version (easy to search, compiled into one file). GPO eCFR

Don't download anything. Instead, search the eCFR (the most user-friendly,

online search tool available from US Government source). Or Compile your own copy of 26-CFR (we'll tell you

how to make a complete copy of all sections from the GPO,

something even they didn't bother to do until late 2004 [2005]...

Not fun, but possible).

There are dozens of GNU-Linux OS, try a

few LiveCDs.

1. Download ISO file.

2. Burn 'image' to disk.

3. Insert CD or DVD.

4. Reboot.

5. Try Linux.

6. Remove CD and reboot again to return to your OS.

Did you know the Income

Tax/Money Scam has been made into a movie?

Aaron

Russo, who made the movies "The Rose" with Bette

Midler, and "Trading Places" with Eddie Murphy, made

a movie that exposes the politicians and their income tax fraud.

* Save PDF images then upload to VistaPrint.com to make your own high-quality short or long sleeve t-shirts.

Data Mining

Tax Law - A computer scientist's guide to finding all “deductions” in the "code."

Here is a secret you are not supposed

to know...

It can be demonstrated (and proven) using any

computer that U.S. Income tax is fraudulently imposed.

According to the code, only "Foreign earned

income" is taxable income. Most Americans

owe nothing! The

"Code" does not lie.

Where are the “deductions”? What's "excluded

income"? What is taxed?

Go

ahead, test a few 'experts.' Ask or email them this

simple question. You should expect accuracy when paying 'professionals'

to perform. Ask your CPA,

or even a law

professor, to provide the section number which defines Exempt

income. Ask the IRS.

Ask a judge.

Ask your tax

software developer. All of these experts should know exactly

where "Exempt income" is defined. It's just

an easy Tax-101 question, but it's their job to know it.

Because statutes and regulations are

codified,

a simple search will accurately show every section

written for exclude income, eliminated income, eliminated

items & the legal definition of Exempt income.

Find everything, and anything, ... without an 'expert.'

You can search U.S. tax code using your computer,

or the Government's own search engines, both methods are

described here.

Simply find the "code-words"

which you think are necessary for determining taxable

income, ... do some data mining. You'll soon find Section

861 and will see there can be no misunderstanding ...

U.S. Income tax is a scam implemented under

color

of law by politicians and bankers.

Fact: Exempt income is legally defined in Sec. 861, and, according to "code", only "Foreign earned

income" is taxable income.

1. Code of Federal Regulations

The "code" in the Code of Federal

Regulations has many instructions and code-words which are written

in just one section (leaving little room for doubt or

uncertainty).

Fact: These tax instructions are only written in Sec.

861...

"how to determine taxable income"

"eliminated income"

"eliminated items"

"specific sources"

"specific guidance"

"the sources of income for purposes of the income tax"

"income that is exempt or excluded"

"exempt, eliminated, or excluded income"

<i>exempt income</i> (include HTML characters)

“exempt income” (include all characters)

“deductions” (include all characters)

"deductions to excluded income"

"income that is not considered tax exempt" (i.e. taxable

income)

Confirm

with the Source: Government Printing Office http://ecfr.gov

Among thousands of sections of law, these

instructions & code words are found in just one section

- 861. There are more search results like these, including

several boolean search results, in tax regulations

and statutes. All results have

one thing in common - Section 861.

Why Section 861 ?

The most basic and fundamental objects in taxation

(and/or their instructions) are written specifically in

section 861. Obviously, such basics would include the rules...

for determining taxable income, gross income, exempt income,

excluded income, eliminated income, ...and rules for expenses,

losses, deductions, and the allocation of each

of these. In fact, only section 861 has all of these.

Fact: Required "code" is prescribed

specifically within Sec. 861 ...

"excluded income"

"gross income may include excluded income"

"deductions to gross income"

"the rules... for determining taxable income"

(use Boolean search)

"allocation

and apportionment of deductions"

"allocation and apportionment of expenses"

"allocation and apportionment of taxable income" (see Sec. 863-2(b) referring to 863-1 referring to 861-8)

"allocation and apportionment to exempt, excluded, or eliminated

income"

"exempt, excluded, or eliminated for federal income tax

purposes"

Evidently,

the IRS knows how to data mine your info, but they can't bother

to data mine their own regulations.

'Tax Experts?'

... Pffff!

... Turbo Tax, H&R Block, TaxAct, etc ...

... Aren't you just frauds?

Where is "Exempt income" defined in tax law?

Have none of you 'tax experts' ever

thought to ask this simple question? Certainly, many of you

found this long ago, but kept very quiet ... Where

did you get your code? Who gives it to you?

How do 'tax experts' calculate income taxes without

using "the rules ... for determining taxable income"?

How does your tax software calculate deductions

without using the code written for the "allocation

and apportionment of deductions"? What, nobody

has deductions?

How about the "allocation and apportionment of

expenses"? ... Nobody has expenses?

How about "allocation and apportionment of taxable

income"? ... What the hell?

How does tax software, such as Turbo Tax, TaxAct, and

H&R Block, even function, if it doesn't consider

"excluded income", "eliminated income",

"eliminated items", "exempt income",

... or the income that is not ... exempt?

... to find the legal definition of Exempt

income?

How

is it that nearly all of you can spend your entire careers involved in

taxation but not bother to find this basic definition?

"How terrible it will be for you experts in the law. You have taken

away the key to knowledge. You didn't go in yourselves, and you kept out those who were trying to go in."

- Luke 11:52 ISV

Taxable or Exempt (it's only as complicated

as day or night) ... Other 'experts' can be understood, "so

interested in its profits, or so dependent on its favours that

there will be no opposition from that class," but

law professors? What the hell? You suck! Evidently, truth is not your

religion.

"How fortunate for leaders that men do not think."

-- Adolf Hitler

Fact:"Exempt income" is legally

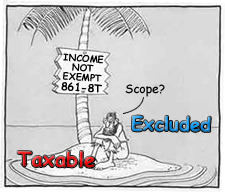

defined in Section 861 ... Thus, 861 can never be frivolous.

"(ii) Exempt income

and exempt asset defined

...the term exempt income means any income that is ...

exempt, excluded, or eliminated for federal

income tax purposes." -

26

CFR 1.861-8T(d)(2)(ii)

Taxable income is specified after Exempt is defined...

"(iii) Income that is not

considered tax exempt. The following items are not considered

to be exempt, eliminated, or excluded income" -

26

CFR 1.861-8T(d)(2)(iii)

Only Section 861 prescribes the two most important

items for any income tax...

1. Exempt

income

"exempt income means any income

that is exempt, excluded, or eliminated..."

2. Taxable income

"Income that is not ... exempt." (taxable

income)

You can confirm section 861 using the government's own search

engine http://ecfr.gov

Click on Simple Search >> Enter

Title 26 >> Search for:

excluded income (13 matches*)

eliminated income (4 matches*)

eliminated items (1 match*)

specific sources (3 matches*)

specific guidance (1 match*)

how to determine taxable income (2 matches*)

exempt income AND defined (40 matches*) - Use boolean

search

*Results from year 2008

Notice... Section 861 is not frivolous.

Statutes and regulations do not say what you think

and Ignorance of the law is no excuse.

Two Kinds Of Income

Ultimately, you will find there are only two (2) kinds

of income... 1.

excluded income

2. taxable income

Ultimately, income will be taxed, or it will be excluded

(exempt).

Taxable income (Income

not exempt)

It's no secret, it's even written in Form 1040 Instructions

provided by the IRS. And it's prescribed by law in regulations

...

Many IRS

agents have been trying to tell you for years, it's a fraud.

But, that doesn't make the news. According to data mining

with government search engines, the actual income tax

law is found in 26 CFR 1.861-8T

Exempt income is "defined" in 1.861-8T(d)(2)(ii)

Taxable income is prescribed as "Income

that is not considered tax exempt"

in Sec. 1.861-8T(d)(2)(iii)

You can confirm anything your 'tax expert'

tells you, and you can verify everything written here

at WhatisTaxed.com, quickly. The law is codified ...

the results are the same for everyone.

Many code-words verify that Sec. 861 prescribes

the list of taxable income, exclusively. According to the list,

Americans are being scammed - only "Foreign earned

income" is taxable.

Don't

believe it?

"The following income tax returns shall be filed"

(1 match) - Sec.

6091-3

(Search with ecfr. Use

'Simple Search', No quotes)

Notice, it's all foreign.

But it gets worse, Slave.

Did you know

Federal Income Tax does not pay for

any government services...

No roads, No schools, No fire dept., nothing!

No roads ... No schools ... No fire

departments ... Nothing!

This is not fabrication. In 1984, a government report

stated...

"100% of what is collected is

absorbed solely by interest on the Federal debt and by ... transfer

payments. In other words, all individual income tax revenues

are gone before one nickel is spent on the services which taxpayers

expect from their Government."

-- Grace

Commission Report (PPSS) - Ordered by, and submitted to

President Ronald Reagan on January 15, 1984 (wiki)

Fact: "100% of what is collected is absorbed"

According to the U.S. Government, the Income Tax does

not pay for our government services... "all individual

income tax revenues are gone before one nickel is spent on the

services".

Evidently, something

else covers the cost of government services.

2. The United States Code

Do

you think Sec. 861 is just a fluke or coincidence? All the search

results shown so far come from regulations, but data mining

can also be performed on tax statutes found in 26USC.

A powerful data mining technique known as a boolean search

makes it possible to find every statute having

all of your desired "code-words".

Search using the government's own search

engine...

Politicians and bureaucrats claim

that following Sec. 861 is frivolous.

Sec.

861 may be the only law which the Government does not

want us to follow.

The code contradicts the politicians and judges.

But, because U.S. Federal Income tax has been codified,

it is possible to find every law, rule, and instruction

for any subject by using a computer. And, it can be

done fast and easy. You will be able to determine exactly what

is written, and what is not. There is no need to trust that

your 'tax expert' has actually read the tax law and knows what

he or she is talking about. (You've probably seen news stories

before, where "x" number of 'tax professionals'

were hired, they got "x" number of results.)

Learn how to search laws yourself, because

you are ultimately held responsible for your taxes,

anyway.

Politicians

and bureaucrats imply "all income" is taxable.

However, you'll see the law states, "Except as otherwise

provided". You'll find it "provided"

in Title

26, CFR Sec. 1.861-8T(d)(2)(iii). See it In

a Nutshell. Find out exactly what you've been commanded

to do (shall), and what you have not, ... under any

Title of Law. If the laws, or rules, in your country have been

codified, nothing can be hidden.

The data mining results cannot be faked. Force

yourself to look, it's a duty to know the law, Ignorance

is no excuse. You just won't believe it until you see it

with your own eyes. Be sure to utilize a computer's precision,

it'sthe only appropriate code tool.

According

to the US Tax Code, and the Code of Federal Regulations,

most U.S. citizens don't owe any federal income

tax.

According to the list of income not exempt,

which is located in CFR Sec. 861-8T(d)(2)(iii), only foreign

earned income is taxable income. This is not just an opinion,

it is digitally-precise fact. All you need to do is search the

law, to see what is written, and where it

is written.

Three Standards of Proof

In the U.S. courts, there are three

standards of proof - 1) Preponderance of evidence,

2) Clear and convincing evidence, 3) Beyond reasonable

doubt. Each standard is easily met. Prove it to yourself.

Nothing

is for sale at WhatisTaxed.com We do not promote anything or offer any tax

advice. You'll just have to follow the laws yourself. But, if

you use the code, and a

computer, you'll find that judges, politicians, and so-called

'experts' are ignorant, or pretending to be, and illegally taxing

and scamming Americans under Color of law.

Tax Rule No. 1 : "The

tax imposed is upon taxable income"

[Title 26, Code of Federal Regulations, Sec. 1].

So, search for taxable income ... and use the Government's

own search engine

"how to determine taxable income"

(1 regulation. What's the section number?)

"the rules" AND "for

determining taxable income" (1 reg.) [Boolean

search]

"taxable income" AND

"specific sources" (1 reg.)

"taxable income" AND

"specific guidance" (1 reg.)

"income for purposes of the income

tax" (1 reg.)

"income that is not considered

tax exempt"

[income not exempt, i.e. income that is taxable]

(1 reg.)

Or, have your computer show you

All the rules for "excluded

income" (7 regulations)

instructions for "allocating deductions"

(5 regulations)

All the rules for "eliminated

income" (2 regulations)

The rule for "eliminated

items" (1 regulation)

"excluded from gross income entirely"

[showing "more common items are... excluded"]

(1 regulation)

"income that is exempt or excluded"

(1 regulation)

There are more like this. Search for any code-term

that you have determined is necessary, or even reasonable, for

a computation of tax. You'll soon become very familiar with...

"the rules

[of Sec. 861] for determining

taxable income"

According to the Code,

the US Income Tax is a fraud, and Color of law.

This simple method of searching applies to

all Laws (Homeland Security, Banks and Banking, Food and Drugs,

Judicial Administration, Money and Finance: Treasury, etc),

and to their Regulations, or anything else codified.

* The research published here (who and what

is taxed) assumes there already exists proper authority, jurisdiction,

citizenship, being an employee, earning wages, etc. But here

at WhatisTaxed.com, even the 16th amendment is assumed

legal. Of course, all of these conditions have major problems,

and could be the topics of their own websites. This website

is about What is taxed, & excluded, and

assumes we are all subject to the tax imposed.

Income Tax?

Obviously,

tax rules should contain:

1) A list for what is taxed

2) Instructions for how to determine tax

These are required, so people will know exactly what is excluded,

deducted, or taxed. Isn't that the purpose?

Fact: Only 1 regulation, Sec. 861, provides the

following:

"specific guidance"

"specific sources"

"the sources of income for purposes

of the income tax"

"Income that is not considered

tax exempt." [i.e. income that is taxable;

taxable items.]

The definition for "exempt income"

"eliminated income"

"determining taxable income of the

taxpayer"

"determining taxable income from

specific sources"

"how to determine taxable income"

[Why do you think this isn't Tax Rule No. 2, but instead is

found near 6000 pages later in the 9th Volume? Why hide such

an important instruction?]

Many one-of-a-kind instructions, cross references, and even an

index tell people to use Sec. 861 to determine tax. Why are these

ignored?

Remove all ignorance, doubt, and lies by data-mining the tax

code - the Code of Federal Regulations and US Code.

Find any rule in the book.

"Income that is not considered

tax exempt"

See exactly what is taxed.

Many people know there is taxable income,

and non-taxable income, but the regulations say,

"The tax imposed is upon taxable income" (1 file).

According to "the rules... for determining

taxable income" (1 file),

only foreign earned income is taxable income for a U.S. Citizen.

Where

are the Rules?

"the rules": (1338 files found)

"taxable income": (817 files found)

"determining tax": (49 files found)

"determining taxable income": (29 files)

"determine taxable income": (6 files)

"the rules...for determining taxable income"

(1 file found) 26 CFR Sec. 863-1(c)

Among the millions of words in the tax law, in statutes

and regulations, this prescription occurs only once.

It says the rules are located in Sec. 861 and the

regulations thereunder.

If "the tax imposed is upon taxable income",

then most Americans owe ZERO.

The United States tax laws almost completely contradict the IRS.

So, which one is broken?

This is not a tax scam promotion - nothing is sold. Do

not believe anything we tell you, it is far too easy to see it

for yourself. This is only research (easily repeatable) of what

is actually written in tax code, and in the US tax rulebook -

Title 26, Code of Federal Regulations. According to law, you are

reponsible for your taxes, to know all the rules, and to make

your own determination of your taxes. We promote nothing, except

reading tax regulations, and how to search all of the Tax Code

using a computer.

The Real Value = Sight

You may find this tax research shocking, but pay attention...

the real value to be gained here is the simple search technique

being used. It applies to all Titles of regulations and

statutes [all laws], and to any large volume of text.

It means nothing can be hidden from you. You simply need an electronic,

digital copy.

The United States tax regulations, from 1913

- 2004, are also available here for free download. Search them

yourself on your computer. You can compare any of the

current regulations here for accuracy with any source you wish.

We provide exact digital copies of the regulations from the GPO,

but with all of their broken links and missing files repaired.

But...

No need to take our word for it,

and complicated searches are not required to find every

subject. Just use the Government Printing Office search

engine, http://ecfr.gov - Hint:

right-click, open in new window.

Because the US tax system is based on code

(the definition of code is a system), taxable income, excluded

income, eliminated income, exempt income, “deductions”,

allocation of these, etc, are required code-words.

If "exempt, excluded, or eliminated income"

exists, the Code must provide a list, either of

"exempt income", or income not exempt.

'Tax experts?'

Couldn't you also find

• "excluded income"

• "eliminated income"

• "eliminated items"

Isn't that your job?

How about income not exempt

(taxable)?

The least you could do is investigate

by searching through regulations

and statutes.

If you don't know, solve the mystery,

it's your profession...

Act professional

!

According to tax law (U.S. Code, and

Code of Federal Regulations), most Americans don't

owe any income tax. According to Sec. 861, only

"Foreign earned income" is taxable income.

But, the IRS, Courts, and Congress say this is a frivolous

argument.

Is Section 861 frivolous?

Find out.

Start by searching the Code

of Federal Regulations

*Source: Government Printing Office - http://ecfr.gov

Why search tax regulations? - To play by the same rules

as the IRS.

"The Service is bound

by the regulations."

- Internal Revenue Manual, 4.10.7.2.3.4

Search for: [pick something, such as a required code term]

Click submit search

Tax Experts?

Can you be a little more "specific"?

Where is the "specific guidance" written in law

for income taxes?

Search for - specific guidance

Fact - Specific guidance for doing income

taxes is only written in Section 861. It's the only

section that can provide a taxpayer with "specific

guidance" for doing anything.

Coincidence? ... OK.

Where are the "specific sources" of taxable

income?

Search for - specific sources

Fact

- Section 861 is the only section that can prescribe

the "specific sources" for anything.

Coincidence? ... Again? ... OK.

Which section specifies "how to determine taxable

income"?

Search for - how to determine taxable

income

Fact

- Only Sec. 861 can specify to a code follower, human or computer, "how to determine

taxable income".

* Note: Tax law consists of thousands of sections, but only

one section provides this critical & specific

instruction.

Of course, anything is possible and this is probably just

another coincidence. Right? ... OK

Which sections prescribe "excluded income"?

Search for - excluded income

Fact

- Sec. 861 is the first section in all of tax law to mention "excluded income".

Still, a coincidence? ... Excluded income? ... OK

Which sections specify "eliminated income"?

Search for - eliminated income

Fact

- Sec. 861 is the only section having "eliminated income".

Which sections specify the "eliminated items"?

Search for - eliminated items

Fact

- "eliminated items" are only found in Sec. 861.

Another coincidence? ... OK

Where is "Exempt income" legally defined?

Fact

- "Exempt income" is legally defined (codified, this means exclusively) in Sec. 861.

At which point will all of these coincidences become a fact?

Boolean Search

Now use the Boolean search function

(found on GPO left-side

menu) to determine which section numbers contain specific

codes. A Boolean search can use AND/OR which allows us

to confirm, or eliminate ANY possible condition, instruction,

or section that is written... Something like using triangulation

to locate a position.

Triangulate the

code

Where does "taxable income" meet or separate

from "excluded income"?

Why? Because everything has a scope.

Find every section that has taxable income AND

excluded income, because somewhere there is a place

where a difference occurs. These two items, taxable

income and excluded income, share a boundary,

a border. This provides for their definitions. Like property

and property lines, these two incomes must separate

at some point, each has a scope. It is not difficult to

find their exact point of separation.

Search for -

taxable income AND excluded

income

Fact - Taxable income and excluded

income separate, or meet, in Sec. 861-8T, exactly between

paragraphs (d)(2)(ii) and (d)(2)(iii). Thus, the difference

between taxable and excluded is prescribed

exactly in section 861-8T.

Tax Professionals?

It's worth asking again, Which section defines "Exempt income"?

Search for - exempt

income AND defined

Fact: Exempt income is "defined"

in just one section of law, just prior to the list of taxable

items...

Sec.

861-8T(d)(2)(ii) - Exempt Income

"Exempt income ...

means any income that is ... exempt, excluded, or eliminated"

Don't believe it? The result can be verified with several

"code-words", so ...

Pick a target and zero in.

From the GPO'seCFR

>> Click on Boolean >> Enter Title

26

Fact: The following subjects are prescribed (codified)

in section 861. (Frivolous? Think of the odds.)

Search for:

federal income tax AND

excluded income

income tax AND

eliminated income

federal tax AND

exempt income

deductions AND

excluded income

united states trade AND

excluded income

business AND excluded

income

individual AND excluded

income

expenses AND eliminated

income

taxable income AND specific

guidance

exempt income AND eliminated

income AND excluded income

rules AND deductions

AND expenses

sections AND deductions

AND expenses

items AND

taxable income AND excluded

income

sources

AND taxable income AND/OR

excluded income

rules AND

taxable income AND excluded

income

allocating deductions AND

gross income

adding AND taxable

income OR excluded income

subtracting AND taxable

income ORexcluded

income

computation AND taxable

income OR excluded income

statutory AND taxable

income AND excluded income

(referring to statutes, since we are currently searching

regulations)

gross income AND taxable

income AND excluded income

gross income AND taxable

income OR excluded

income

apportion AND taxable

income OR excluded income

allocation AND taxable

income OR excluded income

items AND gross

income AND excluded income

items AND gross

income AND enumerated

(Notice, Sec. 61-1 mentions gross income only

nine times, but Sec. 861-8 mentions it over 200 times.

So, which section provides more "specific

treatment"?)

items AND gross

income AND section 61

(Which is more specific? Sec. 61 or 861?)

allocating AND sources

AND taxable income (4)

allocating AND sources

AND gross income (4)

allocating AND items

AND gross income (3)

etc, etc, ...

Result:

Sec. 861 is not frivolous. It's digitally-precise fact.

* Exempt, Excluded, Eliminated

In case you missed it, excluded income and eliminated

income were used in these searches because "exempt

income" is defined as "any income that is,

in whole or in part, exempt, excluded, or eliminated

for federal income tax purposes." [26 CFR Sec.

861-8T(d)(2)(ii)]

There's more...

Tax

'experts'? How did you code your tax software

without following the code from the

CFR and USC?

WHO INSPECTS YOUR CODE?

What is the

source of your "deductions", and

"excluded income"?

You can't all be ignorant.

How many of you take part?

Judges, IRS, Senators,

and Congressmen, say "861 is frivolous,"

but 'Ladies and Gentlemen,' you're lying.

Your own code reveals you as frauds.

Explain

yourselves

The Politician

by Red Skelton

All of these are

located in Sec. 861

(Title 26)

Proximity Search

Now try the GPO's Proximity Search,

which can locate your "code-words" within so

many characters of each other. This shows the code-words that

might be used together to form a sentence (as in a rule or command).

Click on Proximity Search >> Enter Title 26 >> Search

for

(Use default settings, within 80 characters)

excluded income NEAR gross

income

excluded income NEAR items

income NEAR not

NEAR tax exempt (i.e. income

that is taxable)

items NEAR not

NEAR tax exempt (i.e. items

that are taxable)

income NEAR eliminated

NEAR for federal income tax purposes

rules NEAR deductions

NEAR taxable income

rules NEAR for

NEAR determining taxable income

taxable NEAR specific

NEAR sources

taxable NEAR specific

NEAR activities

exempt income NEAR means

exempt income NEAR defined

tax exempt NEAR income

not NEAR tax

exempt NEAR income

statutory NEAR taxable

income

allocating deductions NEAR

gross income

allocating NEAR gross

income

allocation NEAR excluded

income

allocation NEAR taxable

income

allocation NEAR exemptions,

within 120 characters

statutory NEAR excluded

income, within 120 characters

taxable income NEAR for

all purposes, within 120 chars

etc, etc,...

Result: Sec. 861

There are dozens of such code-terms, or combinations, where the

results only come from Sec. 861.

According to Sec. 61, in the Code of Federal Regulations...

To the extent that another section

of the Code or of the regulations thereunder, provides specific

treatment for any item of income, such other provision shall apply

notwithstanding section 61 [CFR Sec. 61-1(b)]

Fact: There is no other section of the Code, or regulations,

that is more specific than 861.

Try searching for your own terms after you've written down several

that you believe are accurate, or reasonable.

REASONABLE?

Simple Search

Now try GPO's Simple Search. Click on the eCFR'sSimple Search >> enter Title 26 >> search for:

how to determine taxable income

Result:Only Sec. 861 prescribes "how

to determine taxable income".

Coincidence?

Now, search for:

income that is exempt or excluded

Result:Only Sec. 861 prescribes "income

that is exempt or excluded".

See if there is any income which has been eliminated

for federal income tax purposes.

Search for:

eliminated income

Result:Only Sec. 861 prescribes which

income is "eliminated income".

Among millions

of words of legal mumbo jumbo, the required topics are

prescribed in Sec. 861. Section 861 isn't frivolous.

There are many more.

Here are a few eCFR search examples that were saved:

Whether it's taxable, gross, excluded, deductions, expenses,

trade, business, individual, eliminated items, or ... the

rules for determining any of these, section 861 is the

result.

How many times must we see section 861 before rejecting the 'coincidence'?

Oh... is that you?

Here are some more results, and more,

or these,

or these,

or try any subject (code-term) that you wish.

Fact: Only Sec. 861 defines "exempt

income", and only Sec. 861 has the list of taxable

income ("income that is not ... exempt").

The tax code is specific. That's the way code is. And, the instructions

provided by "the rules [of Sec. 861] for determining taxable

income" are clear. According to statutes, and regulations,

not all sources, or items of income are taxable

for every individual.

Any 'expert' can show you that taxes come from

"whatever source" [Sec. 61] ...

But, that's true only for...

"Gross income"

"...unless excluded"

...and notice, "more common items...are...excluded

from gross income entirely" - Sec. 61(b)

Simple Questions for 'tax professionals' and

'experts'

Is the tax imposed upon "taxable income"

or "gross income"?

Is the purpose of tax rules to tell users "how

to determine tax" and to "list"

what is taxed?

What is "excluded income"?

What is "eliminated income" and

in which section does it exclusively occur?

In which section is "exempt income"

defined?

Where is the law for the "allocation

and apportionment of deductions"?

What are the rules for the "allocation

and apportionment of expenses"?

Which "common items" are "excluded

from gross income entirely"?

Can people still be called experts, or tax 'professionals,'

without knowing the fundamentals of their craft?

More common items and the unCommon items

are in the code, but the 'code' is not ambiguous. Code is always

precise. Indeed, many machines, including jets, space shuttles,

missles, air conditioners, heaters, power plants, etc, ... (many

systems), even economic empires, would crash, if code was

not precise.

The income tax really does have a limited scope,

it is prescribed in the tax regulations. The Code actually prescribes

- who, where, when, what, and how. Just follow the instructions

in the Code of Federal Regulations, Title 26, step by step, as

written, to see what your own "computation of taxable income"

produces. Despite what previous court cases, judges, or the IRS

may tell you, some things are not frivolous.

People lie, but code cannot.

By searching with your own computer, you can

view only the specific instructions provided by law, those which

have a specific command and a definite action to be performed.

You can filter through the many vague, repetitive, and misleading

general statements, which command nothing definite (often using

words like, "if any", or "unless excluded")

and quickly find the specific instructions for each subject. You

can even ignore all of the numbering of the sections, the table

of contents, the titles, references to references, the other cross

references, and even the index.

See what the commands actually require you to do, with no uncertainties,

no unless this or that, ... No ifs, ands, or buts.

WHAT'S

IN THE CODE?

Read carefully what's behind the following...

"the sources of income for purposes of

the income tax" : (1 file) Sec. 861-1

"how to determine taxable income":

(1 file): Sec. 861-8

"specific sources": (1 file) Sec.

861-8

"eliminated income":

(2 files) Sec. 861-8 and 861-8T

"income that is exempt": Sec. 861-8T

"income that is not considered tax exempt":

i.e. income that is taxable. (1 file) Sec. 861-8T (The

List... which is the whole purpose of a tax rulebook. "The

following items are not considered to be exempt."

Because they are taxable.)

Dozens of similar terms (with 1 file found) produce the same section,

861. See the Search Results. According to the instructions in the Code

of Federal Regulations, the U.S. income tax has been misrepresented

and is more accurately 98% fraud, a lie, and color of law.

Are we being abused? It appears we are slaves, forced to give up to

1/3 or more of our lifes work, rules or no rules.

"The essence of Government is power; and power, lodged as it must

be in human hands, will ever be liable to abuse."

-- James Madison,

Speech at Virginia Constitutional Convention, Dec. 1, 1829

Sec. 861 is the only section that actually

states it has "the rules" which "apply in determining

taxable income... from specific sources... under other sections

of the Code". Look

...

"The rules contained in this section

apply in determining taxable income of the taxpayer from specific

sources and activities under other sections of the Code..." [26

CFR 1.861-8]

No other section, page, or sentence

in the CFR claims to contain "the rules" that

"apply". When "the rules"

are applied, the amount of tax due for most people is nothing.

Don't believe us, just download the tax regulations (the tax

rulebook) and statutes. Read what they clearly say. Unlike some

books, the U.S. Tax Rulebook is not open to interpretation. The

Code of Federal Regulations is specific, as is all code, hence

the name, code.

There is no need to read millions of words. It's the computer

age, take advantage of it. See 'How to Search', or visit the eCFR

and USC

to use the Government's own search engines.

What is Taxed

HAVE

YOU READ THE RULES

?

The scope of the US Income Tax includes

only two things... 1. Foreign earned income (of citizens

and corporations) - whatever source 2. Foreigners - whatever source

Are you a foreigner? Do you make foreign earned

income? The entire U.S. Federal Income Tax applies only

for these two conditions [assuming Title 26 applies at all].

Warning: The GPO doesn't

make downloading the regulations easy, see 'How to Search'

to be sure you get all the rules, or just rely on what

the eCFR tells you, their results match well.

The official online versions of the Code of

Federal Regulations, found on the Government Printing

Office (GPO) website, are incomplete with missing files

& broken links (at least prior to 2004). The TEXT

edition, available here, was compiled from the GPO, but

has broken links repaired. (The GPO uses the same repair

technique, however less completely.)

You are responsible for determining your

taxes. Learn the law. Only a computer and Internet access are

required to verify the income tax is a scam. Download

26-CFR (the rules) and 26-USC (statutes) to your computer to

conduct your own research. Investigate.

The search techniques used here can help you find

whatever you are looking for, in any large work of text - bibles,

company rules, online books, statutes, code, whatever. And,

if it's codified and digital, the answers are quickly yours.

Attention Researchers

If any link has disappeared, try to copy and

paste the link address at http://www.archive.org

-- DISCLAIMER --

The intended purpose of this website, WhatisTaxed.com,

is to data mine with a computer the Internal Revenue Code, and

the Code of Federal Regulations, Title 26, for the "codes" (e.g.

taxable income, gross income, excluded income, eliminated income,

exempt income, deductions, allocation, apportionment, etc),

for rules, and instructions, for determining income tax. The

results have been published throughout this website. It should

be evident these search methods may be applied to any Title

of Law, or large volume of text, and in any country that

has codified laws and rules. See How to Search.

Nothing is for sale at WhatisTaxed.com.

Information posted at WhatisTaxed.com should not be

considered legal advice and is solely for educational purposes.

The reader should not rely on information provided herein to

determine tax.

Do not accept this

website as tax advice.

WhatisTaxed.com is only tax research from data mining tax

law.

To contribute - See How to Search, and Contact

Us.

We do not sell, promote, or advise anything,

but data-mining, searching, and reading tax code with the only

appropriate code tool ... your computer.

We do find every occurrence of a particular

code-term to establish precisely what is written, and what is

not written in tax law. When we say, no other rule

or statute exists - for example, regarding excluded

income, we show you how many files contain this important

code term, and how we searched for it with a computer. You can

easily verify any of the laws, rules, or code-terms in question,

and you should verify every result because it is your duty

to know and follow the law. Ignorance is no excuse.

When searching tax law, we pay close attention

to 26 CFR...

"the Official Interpretation"

"Federal Income Tax Regulations

(Regs) are the official Treasury Department interpretation of

the Internal Revenue Code"

- Internal

Revenue Manual, 4.10.7.2.3.1

Since "the Service is bound," we can be sure that

we are playing by the same rules. It does not require a law

degree to understand them. See How to Search and Search Examples.

U.S. Income tax is a scam implemented under

U.S. Income tax is a scam implemented under

Why Section 861 ?

Why Section 861 ?

How

is it that nearly all of you can spend your entire careers involved in

taxation but not bother to find this basic definition?

How

is it that nearly all of you can spend your entire careers involved in

taxation but not bother to find this basic definition?

Data

mining produced this result in seconds.

Data

mining produced this result in seconds.  Don't

believe it?

Don't

believe it?

Do

you think Sec. 861 is just a fluke or coincidence? All the search

results shown so far come from regulations, but data mining

can also be performed on tax statutes found in 26USC.

A powerful data mining technique known as a boolean search

makes it possible to find every statute having

all of your desired "code-words".

Do

you think Sec. 861 is just a fluke or coincidence? All the search

results shown so far come from regulations, but data mining

can also be performed on tax statutes found in 26USC.

A powerful data mining technique known as a boolean search

makes it possible to find every statute having

all of your desired "code-words".

Sec.

861 may be the only law which the Government does not

want us to follow.

Sec.

861 may be the only law which the Government does not

want us to follow.

Nothing

is for sale at WhatisTaxed.com

Nothing

is for sale at WhatisTaxed.com